Valuation Case Study - Real Estate

Introduction

In November 2022 I stumbled upon an interesting segment of my local newspaper about a real estate property for sale. The investment in question was an appartment of 3 rooms with around 70 square meters of space on one of the nicest streets of our small town. Yet this wasn't any typical appartment for sale, it was a kind of purchasing option that I believe is very unique to France, something called a "Viager Occupé".

The purchasing option is a bit odd in nature, perhaps a bit crude even. Essentially, the option provides the opportunity for an investor to purchase the appartment at a significant discount to its fair value but not have official ownership of it until the owner...welll... passes away. That is, the owner of the appartment, in this case being a 76 year old woman, is using this type of deal in order to continue living in her property until the end of her life (or until she is placed in a retirement home) while also benefit from the significant value of the real estate that she owns. The buyer, on the other hand, is in a position in which they are able to acquire a property at a great discount, but only have delivery of it at an unpredictable point in time. The reason I find this option to be a bit crude is that if the buyer is solely focused on making a profit from this deal, he would, in a way, be speculating on her life. If she lives to a very old age, the investor is stuck and has made a poor affair. If, however, the woman lives only a few more years the investor would have made a great decision and notable profit making opportunity.

I found this to be a very unique and intriguing opportunity. Not because of the profit making opportunity but rather because of the uniqueness of this option and the complexity involved in valuing it. In this section I provide my best attempt at how I would value this opportunity through a cash and costs flow model and the consideration of different circumstances. While my experience in thinking about different investments and economic models is limited, I hope to build on my skills through exercises like this one and continuously improve through repetition and the feedback of others. If you have any comments or pieces of feedback you would like to provide me, please feel free to contact me at: robin.gripon@isn-nice.com

Now for the challenge!

The purchasing option is a bit odd in nature, perhaps a bit crude even. Essentially, the option provides the opportunity for an investor to purchase the appartment at a significant discount to its fair value but not have official ownership of it until the owner...welll... passes away. That is, the owner of the appartment, in this case being a 76 year old woman, is using this type of deal in order to continue living in her property until the end of her life (or until she is placed in a retirement home) while also benefit from the significant value of the real estate that she owns. The buyer, on the other hand, is in a position in which they are able to acquire a property at a great discount, but only have delivery of it at an unpredictable point in time. The reason I find this option to be a bit crude is that if the buyer is solely focused on making a profit from this deal, he would, in a way, be speculating on her life. If she lives to a very old age, the investor is stuck and has made a poor affair. If, however, the woman lives only a few more years the investor would have made a great decision and notable profit making opportunity.

I found this to be a very unique and intriguing opportunity. Not because of the profit making opportunity but rather because of the uniqueness of this option and the complexity involved in valuing it. In this section I provide my best attempt at how I would value this opportunity through a cash and costs flow model and the consideration of different circumstances. While my experience in thinking about different investments and economic models is limited, I hope to build on my skills through exercises like this one and continuously improve through repetition and the feedback of others. If you have any comments or pieces of feedback you would like to provide me, please feel free to contact me at: robin.gripon@isn-nice.com

Now for the challenge!

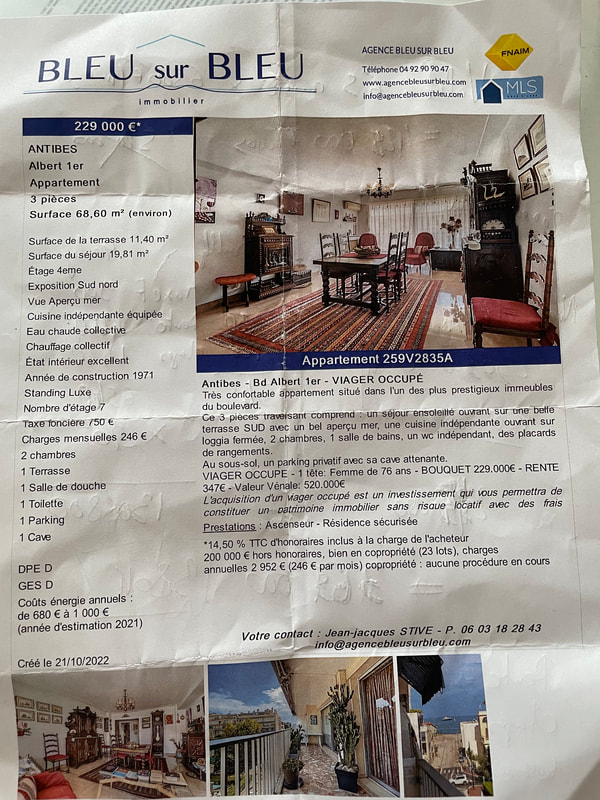

The TermsPictured on the right is a printout I collected at a small local real estate agency that had a copy of the printed flyer for this investment. It presents the terms of the deal, which I have taken the liberty of simplifying and translating into English.

Town: Antibes, France (South of France, which is where my family and I are located) Address: Albert 1er (This street is very large, well known, and well located with many small businesses and markets located closeby. This is of course important to consider when evaluating real estate opportunities). Space Details:

Cost Details:

According to the flyer, the current value of the property, that is if it was sold outright and not as a "viager" (and thus without a discount), would be 520,000 euros. I will make the assumption that this face value is correct, although since there is always some negotiation wiggle room and the acknowledgment of the agency 's incentives, I deem it very likely that this is a large overvaluation (at least of 40 to 60 thousand euros). In any case, for the sake of this exercise I will assume it is correct. |

Figure 1: Flyer of Viager

|

Methodology

|

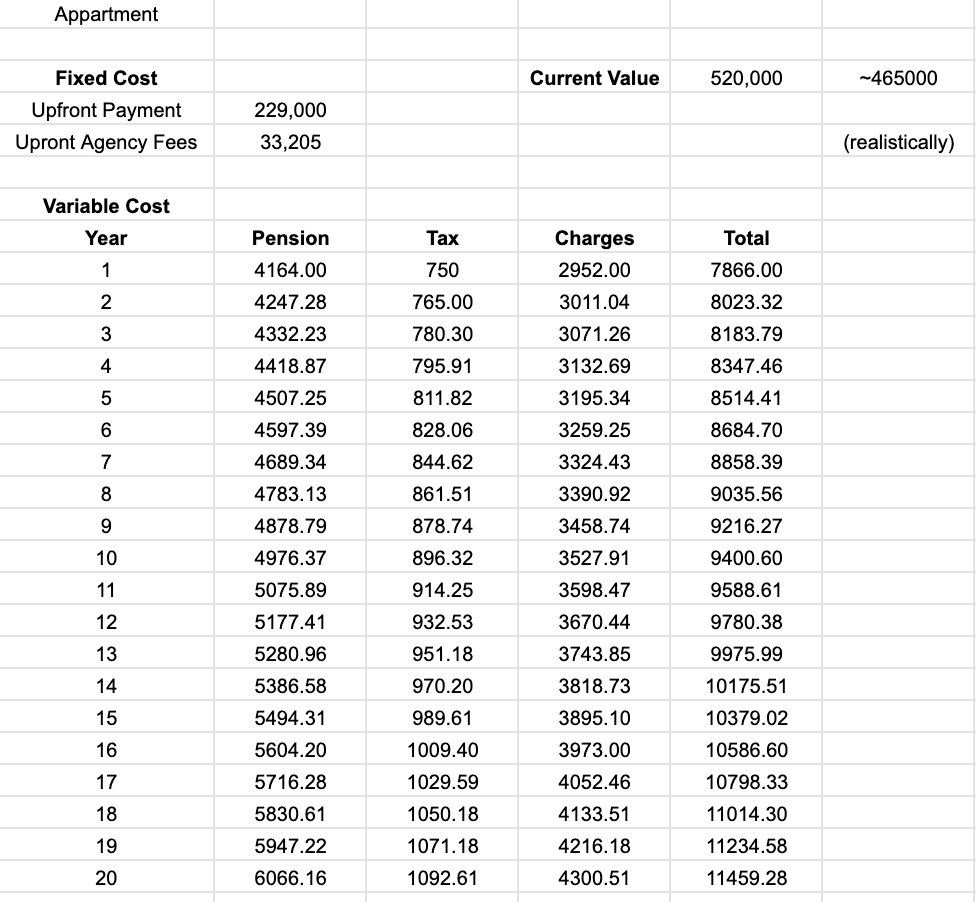

The first step of my valuation model was to lay out the fixed costs associated with this investment. This included the 229,000 upfront payment, and the 33,205 euro upfront agency fees. These are to be paid at the point of investment (aka year 0).

The second step was to lay out the current value of the property determined by the agency. I also include my "realistic estimate" which is based on the belief of the overvaluation because of bias and not based on my knowledge of the property market in my area. Just to be clear. This will be beneficial for me to use as a base to compare the final result of my model with, and thus determine whether this is a good value for investment or not. The third step was to lay out all the variable costs on an annual basis, as per the costs details provided just above. To be precise, in year 1 we have (in euros):

As can be seen all of these are variable cost not only because they are applied every year, they are also set to increase based on the annual inflation rate. In here I am assuming a 2% long-term average inflation rate, based on estimates by the IMF and the fact that it is the traditional target rate by central banks. |

Figure 2: Variable and Fixed Costs modeling

|

|

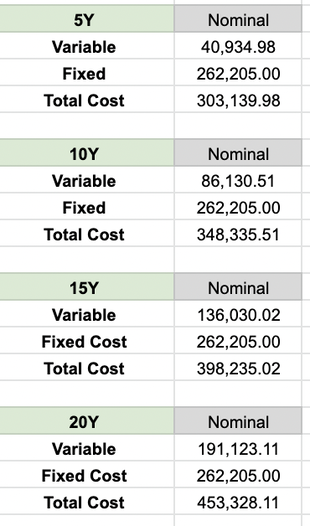

The fourth step of the model is to estimate the costs and final outcomes of this investment For the sake of this project, let me speak about the owner of the property, please accept my apologies for discussing the subject of her passing.

The owner of the property is a 76 year old woman (as seen from the flyer) and is said to be living alone (" 1 tête). I do not have any knowledge of any of her health nor her willingness to go to a retirement home (which is the second way we would get access to the property, apart from her passing). I will also not try to speculate on how long she will live. Although, maybe it is useful to consider the fact that the average lifespan for women in france is 86 years old (so in 10 years). I am, here modeling the different outcomes of our investment based on how long she will live. The fixed cost in all years is 262,205 euros which is, once again, the upfront payment of property and the agency fees. The variable costs on the other hand represent the sums of the total from the table above (Figure 2). Hence, the figure of "40,935" euros shown in "5Y" "Variable Cost" is the sum of all totals (from figure 2) from years 1 to 5. the total costs estimated range from 303,140 to 453,328 euros. All of these are far below the current value of the property, even when accounting for the possibility of it being overvalued. |

Figure 3: Costs over 4 different time periods

|

|

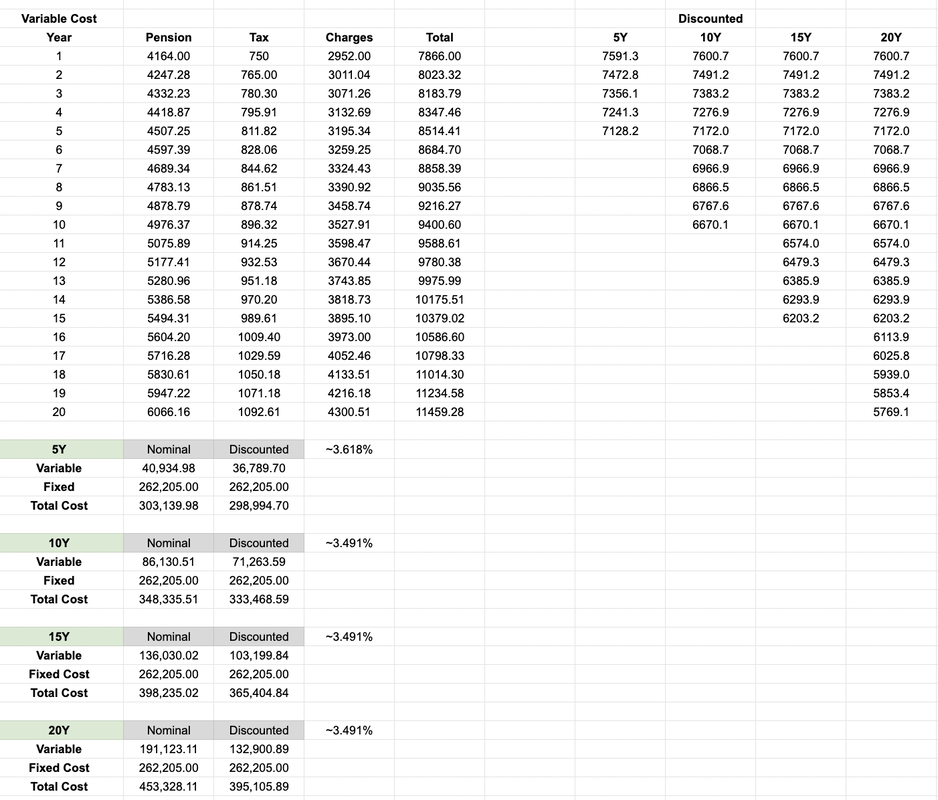

One could be satisfied with this estimate but it would greatly undervalue the investment option. What must be considered is the time value of money: "a dollar today is worth more than tomorrow". It is important, therefore, to discount the annual payments (costs) by a given "risk-free rate". The common rate used in economics is the US government yield. The quotes used here are as of the 15th of December 2022. I am using here the 5-year yield for the 5-year estimate, and the 10-year yield for the 10-year estimates. I, unfortunately, wasn't able to find any data for the 15 and 20 year yield and so I had to satisfy myself with the 10-year yield for those two as well.

As can be seen on the right of Figure 4, I discounted each annual payment by the given discount rate with the following formula: (total)/(1+rf^year). where rf is the risk free rate presented in decimal percentage form (ex: 5% = 0.05). This provides a "Present Value" (PV) of the annual "total cost". I am using these present value payments to be included in the variable cost for each year model in order to give a more accurate depiction of the value of the investment. |

Figure 4: Discounting the Model PV of costs

|

Reflections and Final Thoughts

|

With our method we get the results presented on the right, represented as a present value. These values show that this investment opportunity represents a positive profit making opportunity. This is because the present value of all the costs is lower than the current value of the real estate property.

One could technically take this model further by establishing probabilities of the owner passing away at particular points of time and thus finding a probability weighted value of and expected payoff. These could be done by collecting data on the lifespan of French women (perhaps even women living in the south) and assign probabilities to how long she is likely to live until. However, I find it personally unethical to speculate about someone's death in order to figure out the profit making opportunity of an investment and will thus leave it as it is. I personally found this exercise helpful to think through the complexities of the case study in question, and I hope you also enjoyed reading through how I approached this unique problem. I thank you for taking the time to read through it. If you have any questions, comments, or even feedback, please do feel free to reach out to me at: robin.gripon@isn-nice.com |

Figure 5: Final Payoff Results (Discounted)

|