Investments for the Distant Future - Climate Change

Introduction

Welcome to the first part of my series "Investments For The Distant Future", where I seek to continuously build and further develop a portfolio to position investments to benefit in the very distant future. In this series I look to the long-term global trends that are likely to affect our global economic system and market developments. In this first part of my series I am taking a deep-dive into the topic of Climate Change and how its progression and development will affect markets and how investors, including myself, should be best positioned.

The rise of ESG over the last decade first took place in the world of academia, eventually business, and now in Finance. I remember personally first learning about climate change and its dangers back in first grade. As I grew up the topic of climate change became increasingly ingrained into my schooling with entire units being dedicated to the importance of renewable energy for our future. A number of articles and research papers continue to suggeststhat markets are still not pricing in correctly the climate risks to come. In this there are both physical risks, such as the destruction of real estate in some parts, and transition risks, which are associated with the costs of drastic changes to our current economic system. As things stand, climate associated risks are too far away and our technology not advanced enough for market participants to price in and model these risks and adapt their valuations to a range of different securities.

ESG and its growth is seeking to change that, led particularly by large asset managers, such as BlackRock, and some companies that offer industry disruptive technology offerings, like Tesla. This industry and this change in valuation is certainly beginning to change. I believe this will continue to be the case, and to an even greater level, further on into the future. It is therefore greatly important for investors to adapt their positioning and portfolio to not only avoid these risks and changes, but even benefit from them. This particular portfolio is my first attempt to do so and gain some level of experience in this field.

In this first series, I take a very simple approach to positioning a portfolio for the future of Climate Change. The portfolio is split in two parts and positioned as a pair trade/investment, shorting one basket of securities and going long on another for a neutral position. The fundamental strategy is the following: I am shorting a package of companies that are expected to perform negatively with increasing climate change risks (recognized as "Stranded Assets"), and go long another package of companies that are expected to perform positively in the same futre scenario and have a premium to offer in the future as a result ("Green Premium Assets). While this is a very simple way of investing and developing a portfolio, this is the first part of my series and my understanding of portfolio contsruction will be a continuous learning process as I gain more experience over time.

The rise of ESG over the last decade first took place in the world of academia, eventually business, and now in Finance. I remember personally first learning about climate change and its dangers back in first grade. As I grew up the topic of climate change became increasingly ingrained into my schooling with entire units being dedicated to the importance of renewable energy for our future. A number of articles and research papers continue to suggeststhat markets are still not pricing in correctly the climate risks to come. In this there are both physical risks, such as the destruction of real estate in some parts, and transition risks, which are associated with the costs of drastic changes to our current economic system. As things stand, climate associated risks are too far away and our technology not advanced enough for market participants to price in and model these risks and adapt their valuations to a range of different securities.

ESG and its growth is seeking to change that, led particularly by large asset managers, such as BlackRock, and some companies that offer industry disruptive technology offerings, like Tesla. This industry and this change in valuation is certainly beginning to change. I believe this will continue to be the case, and to an even greater level, further on into the future. It is therefore greatly important for investors to adapt their positioning and portfolio to not only avoid these risks and changes, but even benefit from them. This particular portfolio is my first attempt to do so and gain some level of experience in this field.

In this first series, I take a very simple approach to positioning a portfolio for the future of Climate Change. The portfolio is split in two parts and positioned as a pair trade/investment, shorting one basket of securities and going long on another for a neutral position. The fundamental strategy is the following: I am shorting a package of companies that are expected to perform negatively with increasing climate change risks (recognized as "Stranded Assets"), and go long another package of companies that are expected to perform positively in the same futre scenario and have a premium to offer in the future as a result ("Green Premium Assets). While this is a very simple way of investing and developing a portfolio, this is the first part of my series and my understanding of portfolio contsruction will be a continuous learning process as I gain more experience over time.

Stranded Assets |

|

A stranded asset is a resource, such as a commodity or a set of installations, that is expected to have little value in the future. The term has increasingly been used in the public discourse on climate change and fossil fuels, especially in Europe where there has been research on this area for more than a decade. An example of a stranded asset is a coal mine; while it may currently be producing coal for energy, it is expected eventually lose value as the demand for coal decreases or the mine runs out of coal. In this scenario, an investor could make a profit by betting against the value of the coal mine, for example by taking a short position in the company that owns the mine. The portfolio of stranded assets that I present below aims to replicate this approach on a much larger scale using real companies. Taking on a short position against a basket of companies that are negatively positioned for the green energy shift should lead to positive returns as the risks associated with climate change are increasingly priced into the market.

|

Green Premium Assets |

|

The term "Green Premium" is increasingly used to refer to real estate that meets or exceeds sustainability requirements and thus presents a price premium in value as a result. In this case I am using the term "Green Premium Asset" to refer to an asset that is expected to present a premium in valuation as the market continue to price in the green transition. It can be though of as an antonym to the term "Stranded Asset" presented above. The Green Premium portfolio, therefore, wil consist of companies that are focused on green energy, a sector which is set to increase in value at an exponential scale as the renewable energy shift is put into motion.

Portfolio Construction and Methodology

The approach to portfolio construction presented below is very simple. It seeks to gain some exposure to the two overall themes of stranded assets and green premium assets while creating a net neutral position. The percentage ownership of the two portfolios will be, at first, split equally across a set of 20 companies each. That is, each company will have an exposure of 100/20 = 5%, in the portfolio. More precisely, each company in the stranded asset portfolio will have an exposure of -5%, while each company in the green premium portfolio will have an exposure of +5%. The weighing of this exposure could change as this project evolves, and I develop a greater sense of the best possible approach to gain from the green energy shift, which is the goal of this portfolio.

Progress Reporting

The tracking of the performance of this strategy will start on November 17th 2023. I intend to update the performance of the strategy every 2 weeks by including the raw performance numbers and providing an update of the best and worst performance. The update will also include brief market commentary about the two sectors, as well as any changes that I have made in how the portfolio is positioned.

Limitations

The stranded asset portfolio strategy may have some limitations to consider. Firstly, the portfolio may be more closely tied to the price of the raw commodity, such as coal or crude oil, than to any other factors. This means that the portfolio may experience volatility as the commodity prices fluctuate, and thus not be representative of the effects of the green energy transition in the short-term.

Additionally, as green energy represents a growth sector while stranded assets represent more of a value sector, the portfolio may be poorly positioned based on the current macroeconomic environment. Stranded assets companies often provide attractive dividends as their mature products have great inflows of cash. Whereas green energy companies tend to be at an earlier growth stage and thus tend to be cash strapped as they are continuously investing in their future production capabilities. Due to a higher interest rate level, investors have a preference bias for value exposure over growth. This is likely to be the highest headwind to our portfolio and strategy, especially as we have yet to hit a peak in interest rates both in the US and even more so in the EU.

Finally, while the two portfolios are diversified in their exposure across 20 different companies in each, the portfolio is likely to still have idiosyncratic risks, risk that is associated with a particular company's operations. I recognize this limitation since portfolios developed by hedge funds or asset managers typically have hundreds of stocks instead of just 20 or 40, all in order to eliminate idiosyncratic risks.

Stranded Assets

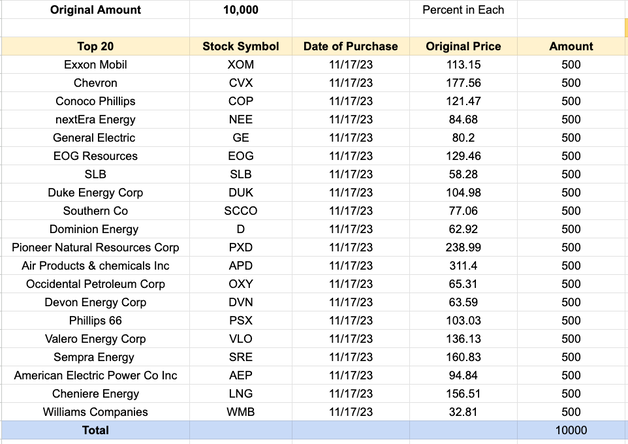

The Stranded Asset portfolio was developed from a list of over 200 companies listed in American stock exchanges that have been given a rating of F by fossilfreefunds.org, a website that tracks the climate impact of companies and mutual funds. The 20 companies chosen were the top 20 largest companies by market cap of the F tier category of companies. Just below is the link of the list aforementioned and below that a screenshot of the companies selected with the price and date of shorting

Link: https://fossilfreefunds.org/fund/vanguard-total-stock-market-index-fund/VTSMX/fossil-fuel-investments/FSUSA002PT/FOUSA00FQU

Link: https://fossilfreefunds.org/fund/vanguard-total-stock-market-index-fund/VTSMX/fossil-fuel-investments/FSUSA002PT/FOUSA00FQU

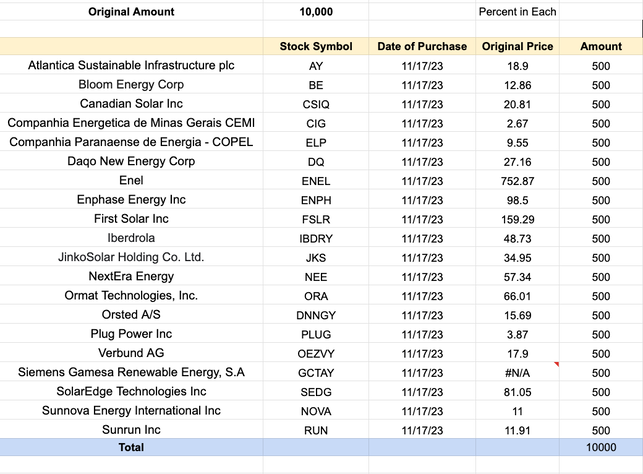

Green Premium Assets

The Green Premium Asset Portfolio was developed from a list of the largest green-only energy companies trading on american stock exchanges. While the list has not been made by a publicly recognized firm or institution, I believe the quality of the sample is sufficient to achieve the exposure goals of this project. Once again, just below is a link of the list aforementioned and below that a screenshot of the companies selected with the price and date of purchase.

link: https://topforeignstocks.com/stock-lists/the-complete-list-of-global-green-energy-stocks-trading-on-the-us-markets/

link: https://topforeignstocks.com/stock-lists/the-complete-list-of-global-green-energy-stocks-trading-on-the-us-markets/